When it comes to applying for credit cards, I put us in the middle of the pack. My wife Sharon and I sign up for enough cards to provide points for most of our trips, but at least one of us I is usually under 5/24.

I try to do as much as I can to keep bank interactions at a minimum. This is primarily because I don’t want to make Sharon get on the phone, which she hates (because she doesn’t know everything about the card she’s calling about and why she applied for it. That’s my job).

Getting to the point, this is why I usually don’t call the bank reconsideration line. For those of you who aren’t familiar with the term, this is the bank department that deals with credit card applications. More specifically, these are the people who look at applications that weren’t automatically approved by the bank’s AI system. If you flunk one of the criteria but aren’t an immediate no-go, your application goes to a human who looks over your credit report, history with the bank, and other parameters to decide if you should be approved for a card or denied.

Don’t immediately call

Many websites tell you to immediately call the bank reconsideration line if you don’t get instant approval for a new card. I’m here to tell you you don’t have to.

While many of our cards get instant approval, as we both experienced with the Capital One Venture X, occasionally, our applications go into pending status. That’s almost expected, with the number of cards we have from AMEX, Citi and Chase.

Instead of instantly calling to find out what’s wrong, I exhibit patience.

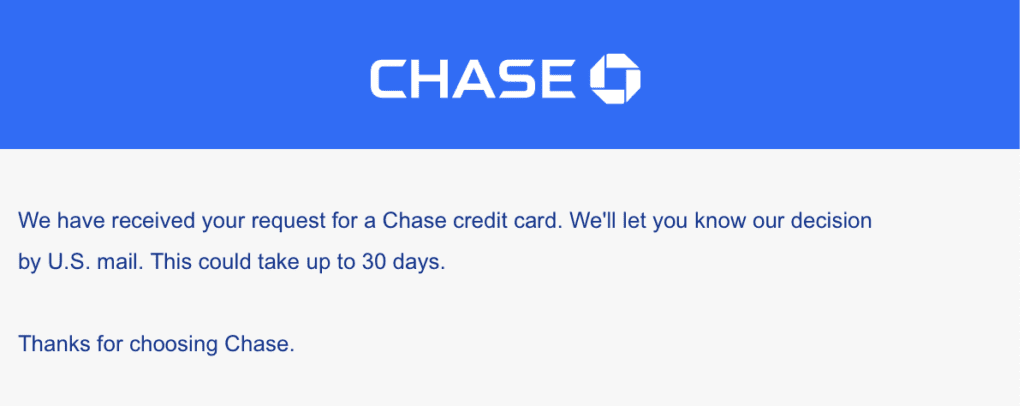

For instance, Sharon applied for a new card from Chase. Much to my disappointment, this was the reply after I clicked send.

At this point, I could have picked up the phone and called Chase, but I wasn’t in any hurry to be approved. I honestly feel that calling a bank is showing your hand. Why not wait for the bank to tell you the problem instead of calling them to plead your case when you don’t even know what the issue is?

In fact, the only time I had a problem getting approved for a card was with the Chase business division when they wanted proof that Your Mileage May Vary was a real business.

Wait for it…

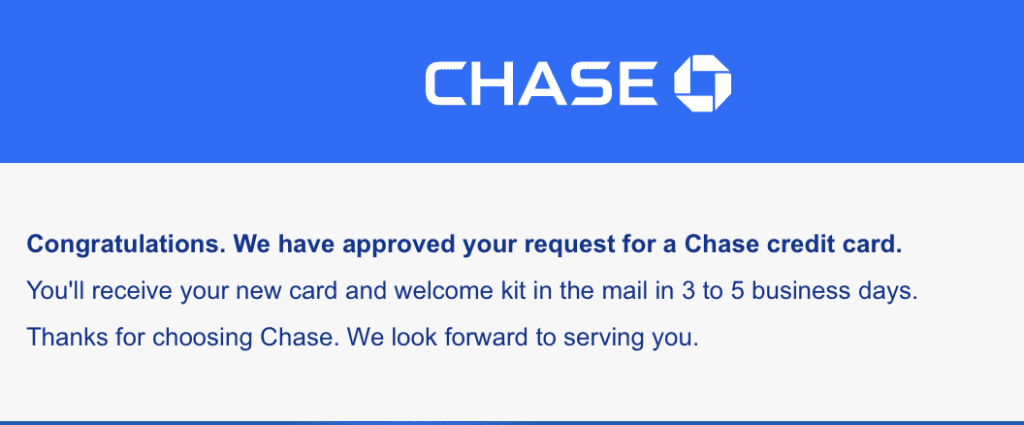

I had time and waited for Chase to contact me. I kept looking online to see if the card showed up in our account, which oftentimes is the quickest way to see when you get approved.

Instead, it was an email from Chase informing me that we were approved.

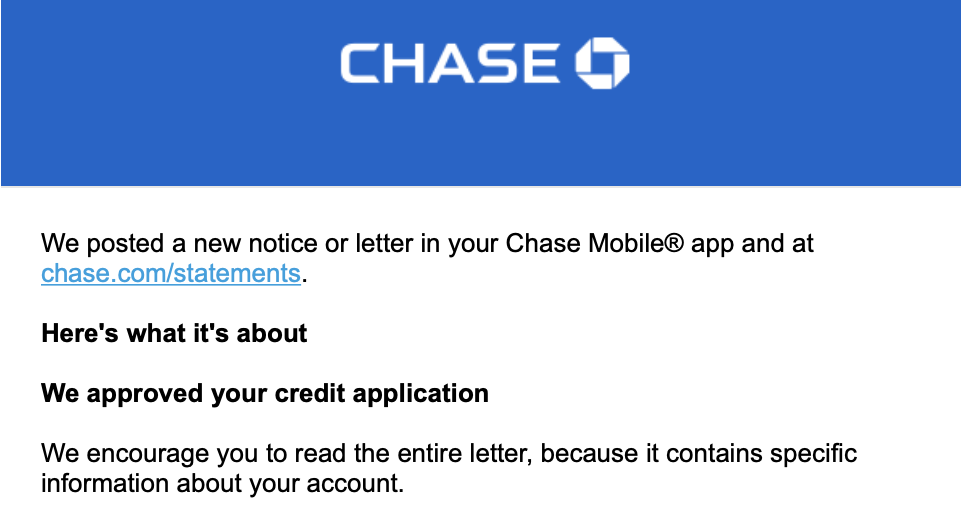

Afterward, I received another email from Chase notifying me that there was a letter waiting in our account.

When I checked, it was a notice that to approve the IHG Premier Card, Chase moved $2,000 from our Chase Sapphire Preferred credit limit.

Apparently, the reason we didn’t get instant approval is that we’ve reached the maximum amount of credit Chase wants to give us. While Chase doesn’t have a number of cards you can hold, they will limit the amount of outstanding credit amongst all of your accounts.

The CSP had a credit limit to spare, and we’d never max out that card. If I had called, I probably would have asked to move 5K to the new card, which would make it easier to meet the spending requirement without making multiple payments.

I’m not saying calling a bank right away is the wrong thing to do. But it’s an unnecessary step if you’re not looking to use the new card right away. Oftentimes, banks find a way to get you approved for a card without you having to speak with them at all.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

Join our mailing list to receive the latest news and updates from our team.