Perfection. Whether you’re a gymnast, ice skater, high diver, bowler or even a student getting back an exam, there’s just something special about getting a perfect score.

For some in the points and miles world or even those who care about their credit score, there’s something special about getting a perfect credit score. Of course, having a perfect credit score doesn’t get you anything. I’m sure that there are those who would argue that if you have a perfect score then you’re leaving plenty of opportunities on the table.

Having a perfect score doesn’t open any additional doors for offers that a good or great score doesn’t provide. You’ll still be approved, or denied, for credit based on the criteria each bank applies to new requests.

So I never really paid that much attention to our scores, just a causal check every month or so to make sure something funky isn’t going on.

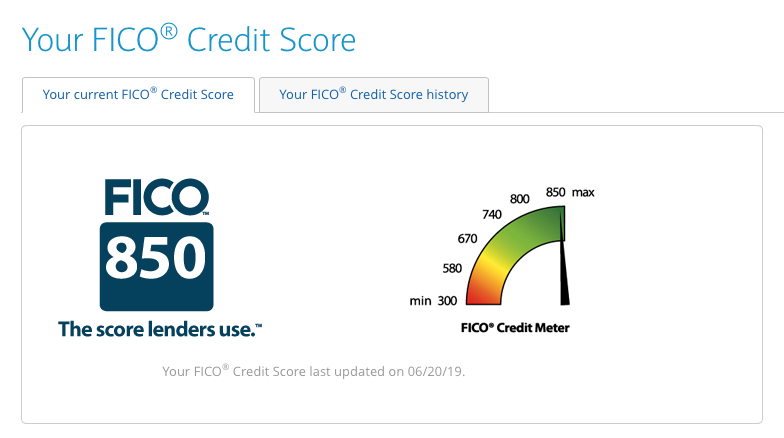

Imagine my surprise when I saw this.

This is a screenshot of Sharon’s FICO credit score that we receive for free from her Barclays account. Barclays shows you the score from your TransUnion credit report, which may be different from the other two credit agencies. Still, even if it is only from one credit agency, a perfect score is a pretty cool thing to have.

Remember, Sharon and I have plenty of open credit cards, two car loans and a mortgage and she still managed to get a perfect credit score. Kinda blows away that myth that opening credit cards will ruin your credit.

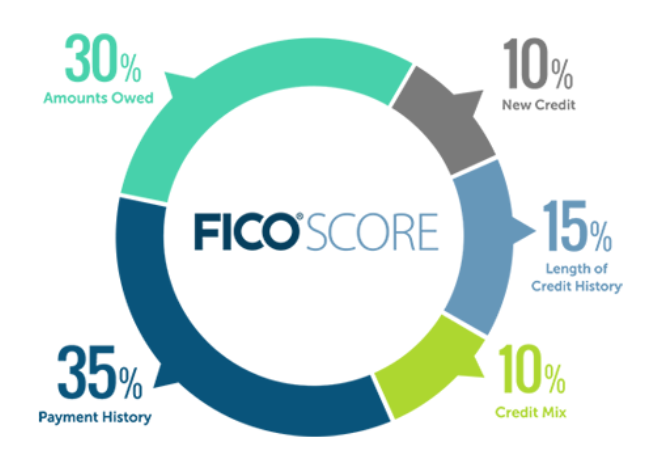

According to FICO, here are the factors that make up your credit score.

- 35% Payment History

- 30% Amounts Owed

- 15% Length of Credit History

- 10% New Credit

- 10% Types of Credit

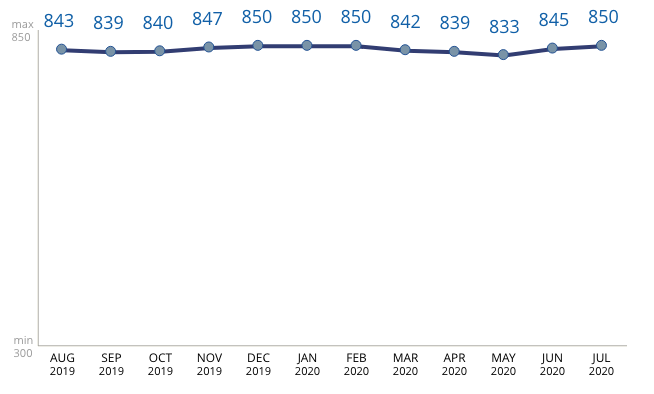

Since first reaching the magical 850 number last year, Sharon’s credit score has hovered between 833-850. The worst month was when she applied for a new card. It took just 2 months to get back up to 850 again.

What do you get for a perfect credit score?

What do you get for a perfect credit score?

Yeah, not that much. Honestly, you need to realize that it’s all downhill after that. You can’t go any higher and any little thing will knock that number down a bit.

That’s OK because we’re not in this game to attain a perfect credit score. While it was nice to have, that was never the goal. I just want to keep our credit scores good enough so that we can keep signing up for credit cards and earning the bonuses. That will keep our balances at a level where we can continue to travel where we want in the style that we want when we’re able to do that again.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and get emailed notifications of when we post. Or maybe you’d like to join our Facebook group – we have 23,000+ members and we talk and ask questions about travel (including Disney parks), creative ways to earn frequent flyer miles and hotel points, how to save money on or for your trips, get access to travel articles you may not see otherwise, etc. Whether you’ve read our posts before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

9 comments

This means exactly 2 things — 1) you are old 🙂 and 2) you haven’t opened enough credit cards lately.

Nope. Someone thought you have to be a senior citizen to have an 850 score. Definitely NOT true. I’m no senior citizen.

It’s not the “real” FICO score. Mine said 837 but when I recently refinanced the true FICO with the various credit bureaus was 817, 820 and 818. Really once you’re over 775 it’s pretty much all the same thing. But kudos as that’s a great credit score but as you mentioned, kind of anticlimactic.

I was just going to post this. The free credit score you get from anywhere is not the credit score that any financial institution uses when you apply for a loan.

Additionally, I have zero debt. I don’t have a car loan, no mortgage payments and I pay off my credit cards in full every month. But my free credit score is 765. I actually just paid off my credit card and my credit score went down 5 points.

As a bank, if I’m debt free and not borrowing money from them, they aren’t making any money off me. As a credit card company, if I rack up money on the credit card then pay it off in full before any interest accrues, they aren’t making any money off me. It really seems like I can have a “very good” credit rating but to get an “exceptional” credit rating, I have to pay some form of interest (mortgage, car loan, credit cards, line of credit, etc.).

The credit bureaus don’t seem to like when you are debt free. Now my bank has an internal ranking they look at along with scores from the credit bureaus. My bank manager tells me they don’t even pull a credit rating on me because I’ve been banking with them for years and they know I’m not a risk. In addition to being debt free, I have investments and savings.

Case in point: my score is 837 (according to the free report via Chase Sapphire and Wells Fargo). But Wells Fargo denied us a Home Equity Line all the same. We got it done through our local Credit Union, which actually turned out to be cheaper and better anyway!

What did you think it would feel like?

I dunno? I wasn’t expecting balloons but a trumpet fanfare would have been nice. 🙂

The credit scores thing seems crazy to me. My score varies between 815-835. Last month, it dipped by 6 points (to 820) because “balances on too many cards”: (I had $30 on Macys from buying a pack of Jockey underwear, and $42 on Amex for some small purchases, and $21 on Citi MasterCard for on-line purchases – all of these get paid off almost as soon as the bill is received)” and “no open mortgage or loan payments” (I paid my home mortgage off 9 years ago, and my wife and I own our two cars, but when they were open we paid all on time). I have NEVER had any late payments on anything. Have about 12 credit cards (Barclays, Discover, Citi, Chase, Amex, etc.) and they all get paid off each month. What astounds me is that buying a cup of coffee on my card seems to lower my score by 5 points, or paying it off so that only Discover has any charges raises it by 10 points. To me this all seems like nonsense. I should be an 850, not an 820. Oh, our combined income is about $300K per year, and our credit card accounts have over $200K in credit available. Go figure these scores …

The scores published by most non credit bureau companies are going to always be lower than the credit scores you find when you get a mortgage or buy a car. The credit bureaus almost always provide scores to a mortgage company lower than what is provided to a private person.Same for automobile credit. I do not know why this is done. This Experian “boost your credit instantly” is basically a mind f—. When one applies for credit this score will almost never appear. ( I hedge my comment because someone will post back that their scores match the “boost your credit instantly” number. I analyzed credit for loans and NEVER saw a credit app where the scores matched. What was provided for the lender to analyze was always lower than what was provided directly to a consumer.)