I’ll admit that I’m not perfect. While I’d like to say that I remember to pay off all of my credit cards every month, it doesn’t always happen. In case I forget to pay off a card, I have most of my accounts set to make the minimum payment before the due date.

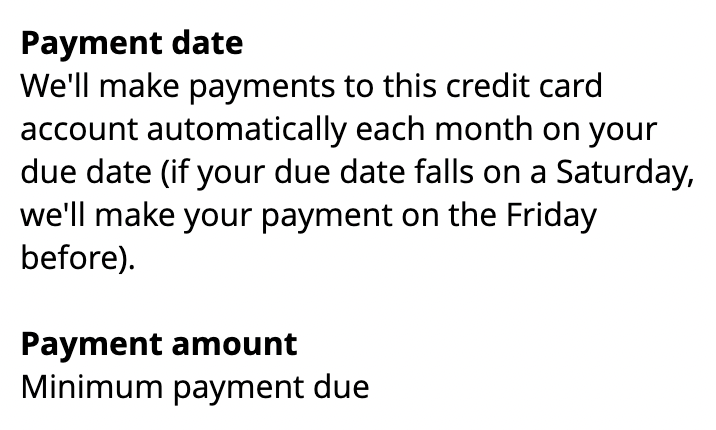

I have my Citi accounts set to make the minimum payment each month. That way if I miss a payment, I’ll only have to pay the interest instead of a late fee.

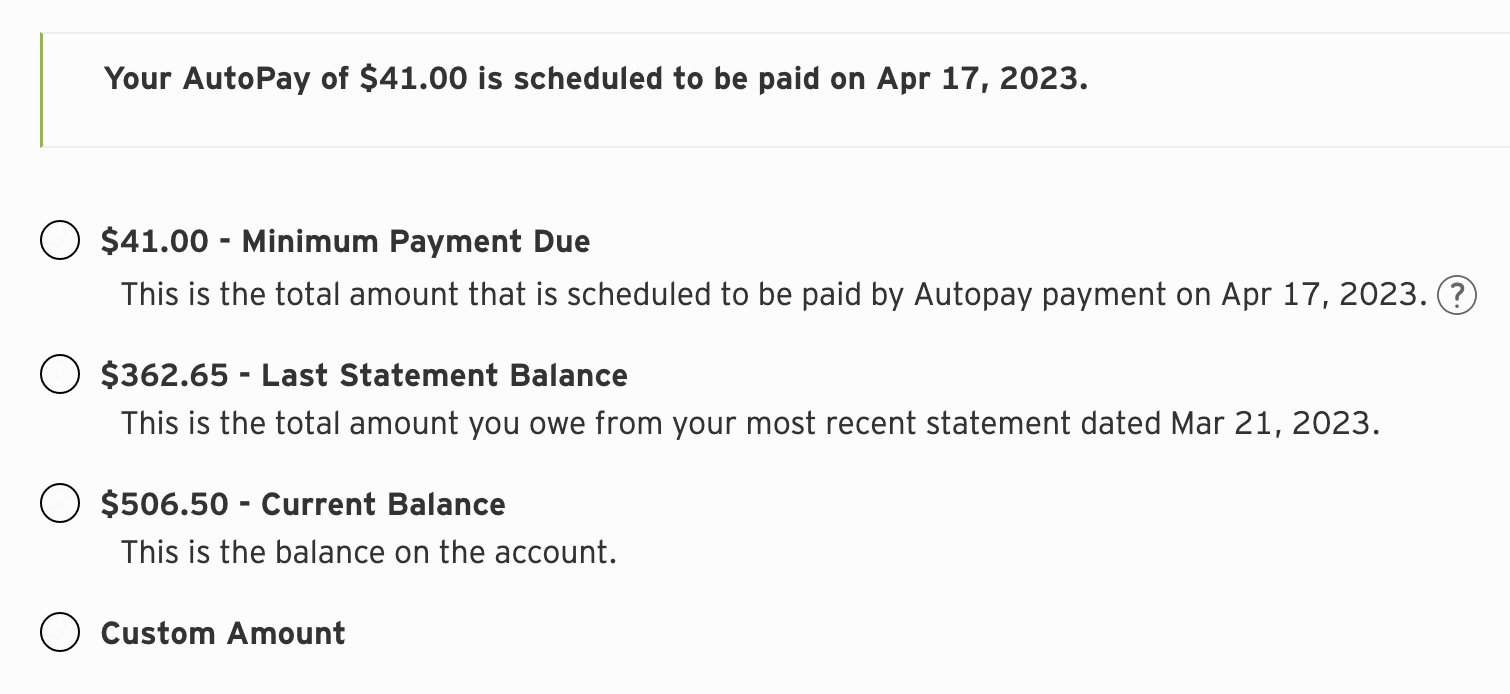

When I pay my Citi accounts, I have an option of what I want to pay. It’s also clear that I have a $41 scheduled payment.

When I schedule my payment for the statement balance, I can see the two payments for my account.

Do you see the “Skip” link which shows next to my AutoPay amount of $41? It’s easy to skip that payment if I have already scheduled the full payment on my account.

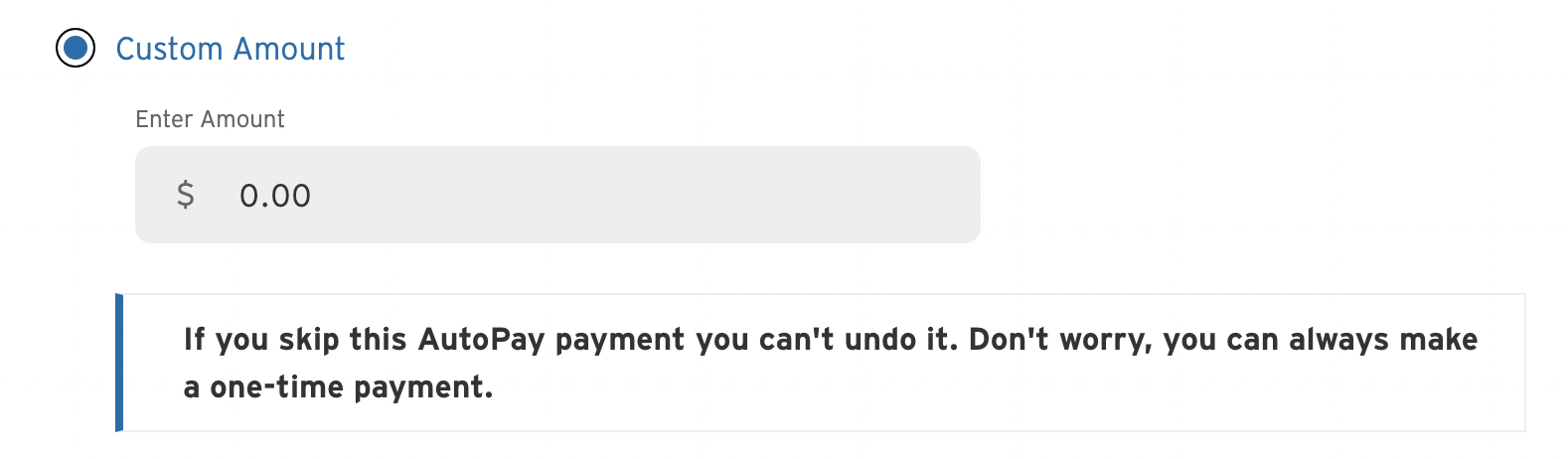

When you skip a payment, Citi lets you know this is a one-time event and that your auto-pay will happen next month.

That’s not what happens when you have an auto payment with Chase. I’ve missed a payment (or three) with Chase so I have set my cards for automatic payment of the minimum payment due.

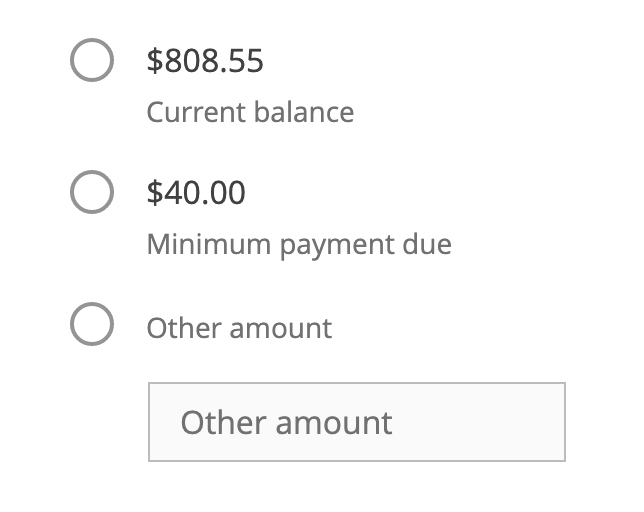

When I go to make a payment, I have the option to pay the current balance, minimum due or another amount.

My card showed that my minimum payment of $40 was scheduled so I set a payment for $768.55 which would pay off the card for the month. However, once I paid the $768.55, the scheduled $40 payment didn’t happen and I have to pay $6.50 in interest charges (because I didn’t pay the full balance).

WTF Chase!

Your website said it would pay the $40 minimum payment so I paid the rest of the bill in advance. Nowhere did you say the scheduled payment would be canceled if I paid the rest of the balance?

Even my Discover card makes it easy to pay the remainder of the balance above my scheduled payment.

Instead, you let me pay for most of my balance but charged me an interest fee because I didn’t pay the entire amount due

I’m upset because I’ve paid the remaining balance due on a Chase card only to have them skip the scheduled minimum payment, leaving me with a balance on my account.

So which is it, Chase? Does paying my account in advance void my scheduled payment or do I have to subtract the scheduled payment from what I pay online? Does it matter when I make the payment?

Any clarity would help when I want to pay my Chase accounts. If Citi and Discover have figured it out, why can’t you?

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

2 comments

No matter how how or when I think I have paid off my Chase card, this includes talking to a representative, I ALWAYS get another bill showing I owe $6 – 13. I then call them back and after a good 20 minutes haggling about it, that charge usually comes off. It’s super annoying. They are the ONLY one I have a payoff issue with. 🤦♀️

I pay all my 23 cards every time a charge posts. Some of my Chase and AMEX cards get paid 15 times or more per month as a few are my heavy lifters. Barclays, Citi, Chase, AMEX, Discover, WF, FNBO, USBank, and a Synchrony card. Why wait until the end of the month? I spin through the apps (and that darn Synchrony website – no app for the Caesars card) every couple of days and pay anything with a balance to $0. Zero out your accounts a couple of times per month and never pay interest. Credit scores are in the 830s, and the points game serves no purpose if I carry a balance. The banks apparently have liked me treating everything for years like a cash card.