It’s been several months since my most recent credit card application. That’s when I applied for an Ink Cash for the 90,000 Ultimate Rewards bonus from Chase. That’s a long time between applications but I’ve been busier burning points than earning them. We’re focused on reaching a spending bonus with the Hilton Surpass AMEX so I haven’t wanted to take on another spending requirement.

In March of 2023, I canceled our American AAdvantage CitiBusiness card. It was time to pay the annual fee and we had no upcoming flights on American Airlines. Since the main perks of the card are preferred boarding and a free checked bag, there was no reason to pay the $99 annual fee. Since Citi offered no retention bonus, it wasn’t hard to let go.

Here we are, a few months later, and I’m about to book a flight on American for this fall. I still want those perks so I looked at which American AAdvantage co-brand card would best suit our needs.

The top tier AAdvantage card from Citi has a $595 annual fee but includes lounge access and has a 100,000-mile bonus if you spend $10,000 in 3 months. I’m not looking to take on such a large spending requirement so I looked to the next tier of AAdvantage cards.

Both Barclays and Citi offer cards with a sub-$100 annual fee that provide benefits of earlier boarding and a free checked bag. I’ve had both cards in the past but it’s been many years since I received a sign-up bonus. I have a healthy balance of AAdvantage miles so a big bonus isn’t important to me right now.

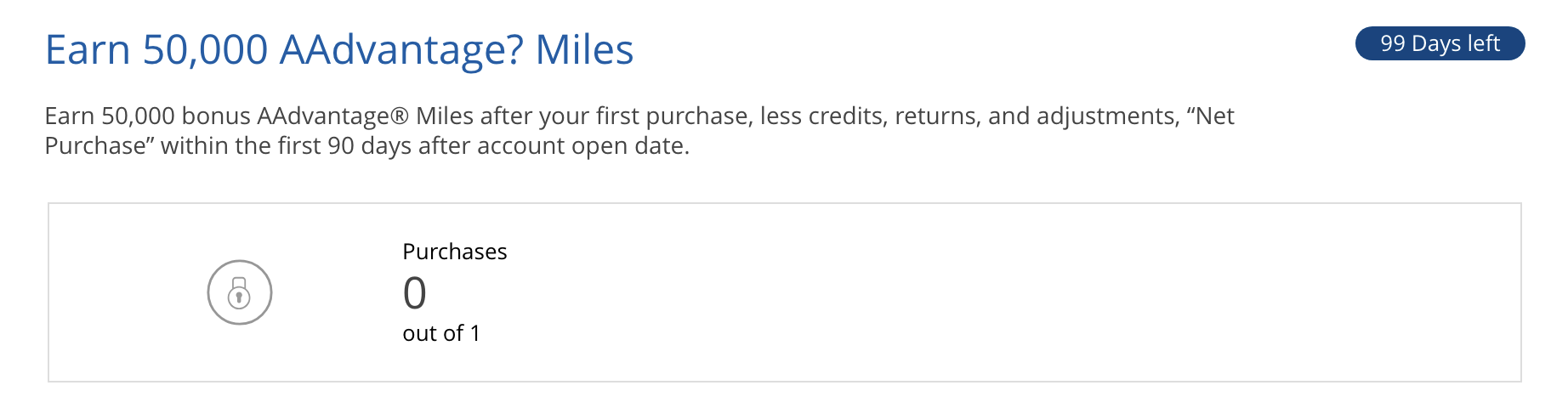

That’s why I decided to sign up for the Barclays American AAdvantage Red card. I found a sign-up offer for 50,000 miles after your first purchase. To make things better, the annual fee is waived for the first year.

Why I Chose Barclays Instead Of Citi

I always like to have at least one card open for both Sharon and me from Barclays. I find this makes it easier for us to apply for new cards from them as we have an ongoing relationship. I account this for why Sharon was able to get approved for a Wyndham Earner Business card with no difficulty.

Currently, my only Barclays card is my JetBlue Plus card. Sharon and I both have one of these cards and while it’s not a bad deal considering we get bonus miles every year, there’s little use for us to both have one. I wanted to cancel mine but I didn’t want to cancel my only card. Getting an AAdvantage Red card would allow me to ditch the JetBlue card.

Why Is This A Risky Move?

Previously I would have no issues about this as it’s been years since I had an American AAdvantage card from Barclays. However, the bank recently added a new caveat to the terms and conditions.

You may not be eligible for this offer if you currently have or previously had an account with us in this program.

I’ve previously had an American AAdvantage co-brand account with Barclays. In fact, I had two cards which were grandfathered US Airways cards. I canceled them when Barclays did away with the 10,000 bonus miles I received each year on my card renewal.

I heard that Barclays Systems didn’t consider these cards as the same as the new Aviator Cards so I decided to take a chance.

Instant Approval

If Barclays determines that I already received a bonus for these cards over a decade ago and that I’m not eligible for the 50,000 point bonus after my first purchase, I’ll chalk it up to experience.

However, when I signed up for the card I received an instant approval with a 20K credit line.

The card instantly showed on my account.

Why I’m Not Worried About The Sign-Up Bonus

When I checked my account, I saw an award tracker for my sign-up bonus.

Once I receive my card and make a purchase, I’ll learn if I get the 50,000 points. However, the points weren’t the reason I applied for the card. I need the free checked bag for our upcoming flights which will save us at least $100 and the preferred boarding position.

Since the card’s annual fee is waived for the first year, there’s no risk in applying besides an additional application on my credit report. I want to keep in good with Barclays and I intend to keep the card for several years as long as we keep flying on American.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

4 comments

If, as you explain, “there’s no risk in applying,” why do your earlier headline and subheading label it “risky”?

Two different things. I took a risk not getting the sign-up bonus. However, I’m not risking anything because if I applied and was denied, I could have always applied for the Citi card.

To get us to click, and it worked.

Wait, what? Barclays has a true once-in-a lifetime signup policy?