We’ve been part of the Apple ecosystem since the very beginning — we’ve been using iPhones since the original one came out in 2007. Over the years, our house has filled up with iMacs, a Mac Mini, MacBooks, iPads, Apple Watches, and plenty more iPhones. (This is an old photo — we’ve had many more iPhones since then.)

I remember when you could finance a new iPhone through your mobile carrier. With iPhones now costing north of $1,000, being able to roll the cost into your monthly phone bill felt a lot more manageable than paying the full amount upfront.

But starting with the iPhone 13, Apple stopped offering financing — unless you applied for the Apple Card.

I hadn’t planned on getting one, but once I looked into it, I realized the Apple Card had some benefits you just don’t see with other credit cards.

What Is the Apple Card?

The Apple Card, issued by Goldman Sachs, launched in August 2019 as the first credit card fully integrated into the Apple ecosystem. As soon as you’re approved, it’s ready to use in your Apple Wallet. You can make purchases, view transactions, and pay your bill — all directly from your iPhone or iPad.

There’s no annual fee and the card functions as a cashback card. But instead of waiting for your statement to close, Apple gives you Daily Cash — your rewards are credited daily.

All cashback earned goes into your Apple Cash balance in your Wallet. You can use it for purchases, transfer it to friends, or move it to a bank account.

Apple Card Earning Rates

The card’s bonus categories are unique:

- 3% cashback on purchases made directly from Apple

- 3% cashback at select merchants (like Walgreens, Uber, Nike, and others) when using Apple Pay

- 2% cashback on all other Apple Pay purchases

- 1% cashback on everything else (including purchases with the physical card)

While 3% back at Apple or Walgreens is nice, it never felt compelling enough for me to “waste” a card application — until we were planning to spend a decent amount of money on Apple products.

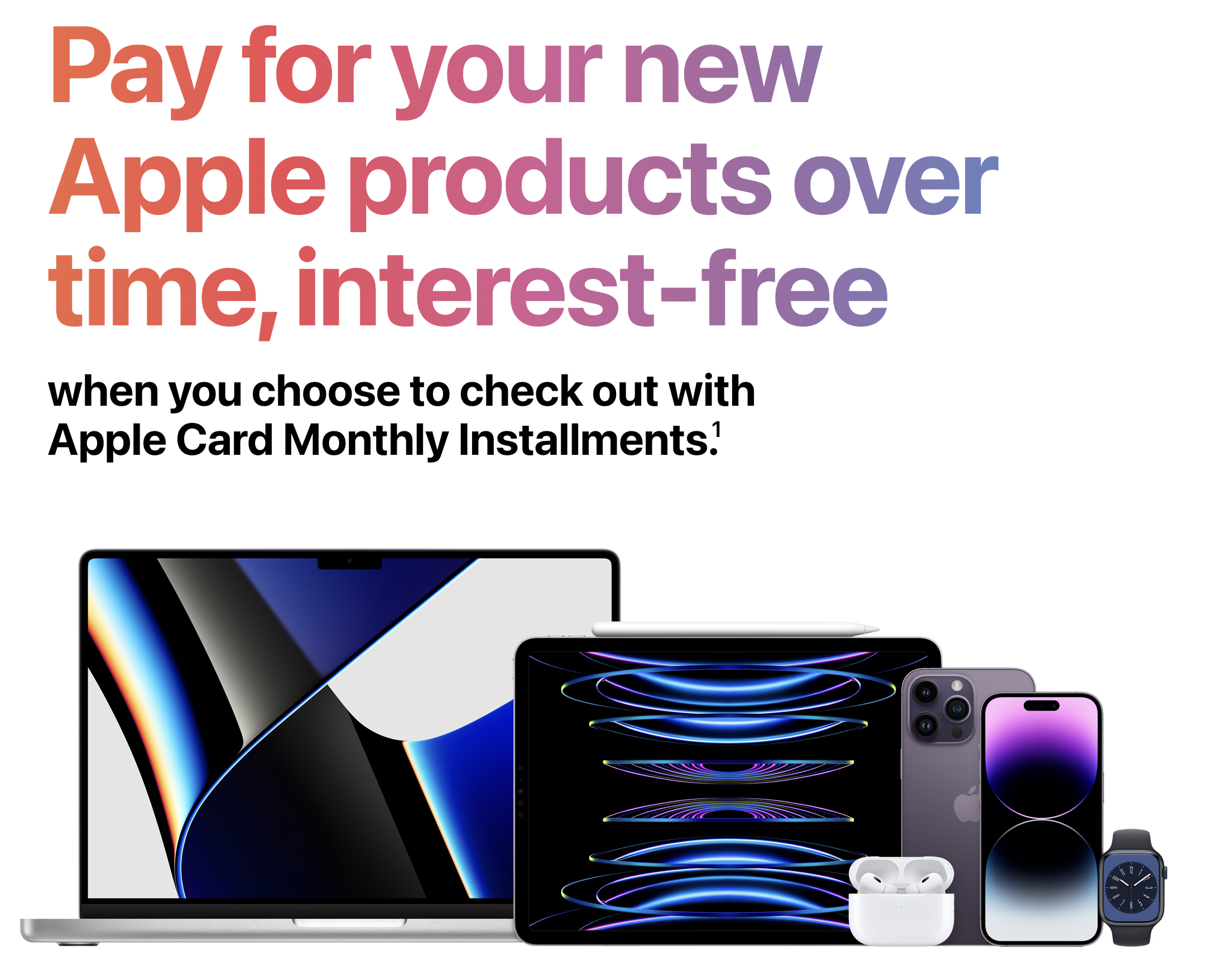

The Killer Feature: Interest-Free Apple Financing

The standout benefit of the Apple Card is interest-free monthly installment financing on Apple products.

When checking out through the Apple Store (online or in-store), you can choose to finance your purchase using your Apple Card. The monthly payments are added to your card balance, and you still earn 3% cashback upfront, even though you haven’t paid in full yet.

That means you start earning cashback before you’ve made your first payment — I don’t know of any other credit card that does that.

I applied for the Apple Card, got instant approval, and used it to buy a new iPhone and Apple Watch. Both times, I was offered the option to pay in monthly installments. As long as you’re logged into your Apple account during checkout, Apple knows you have the card and shows you the financing options.

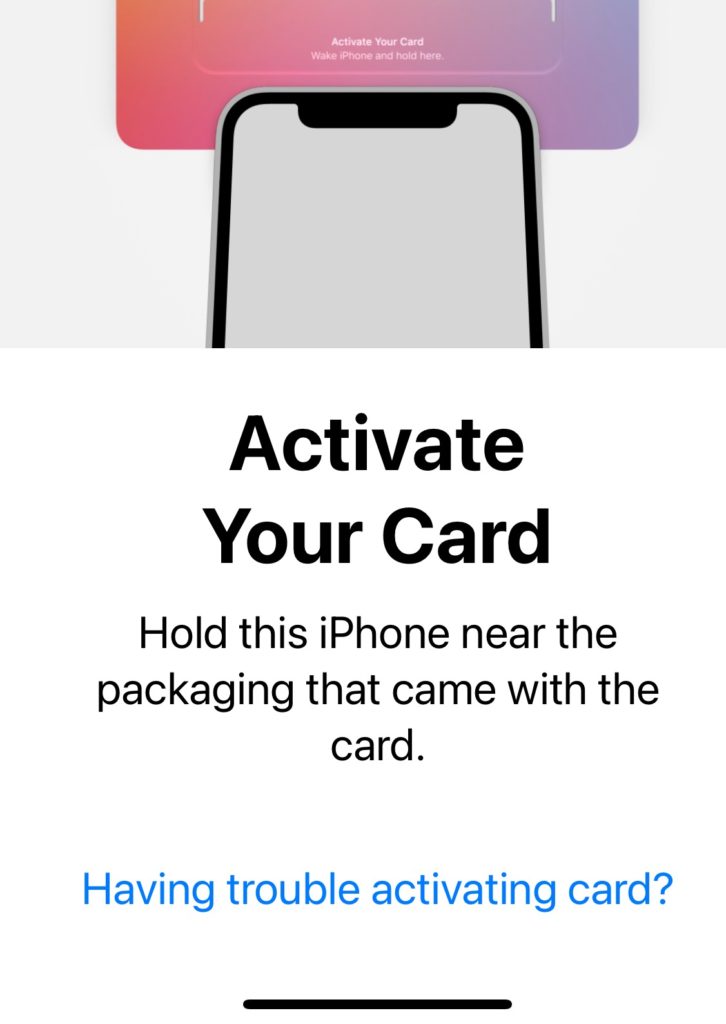

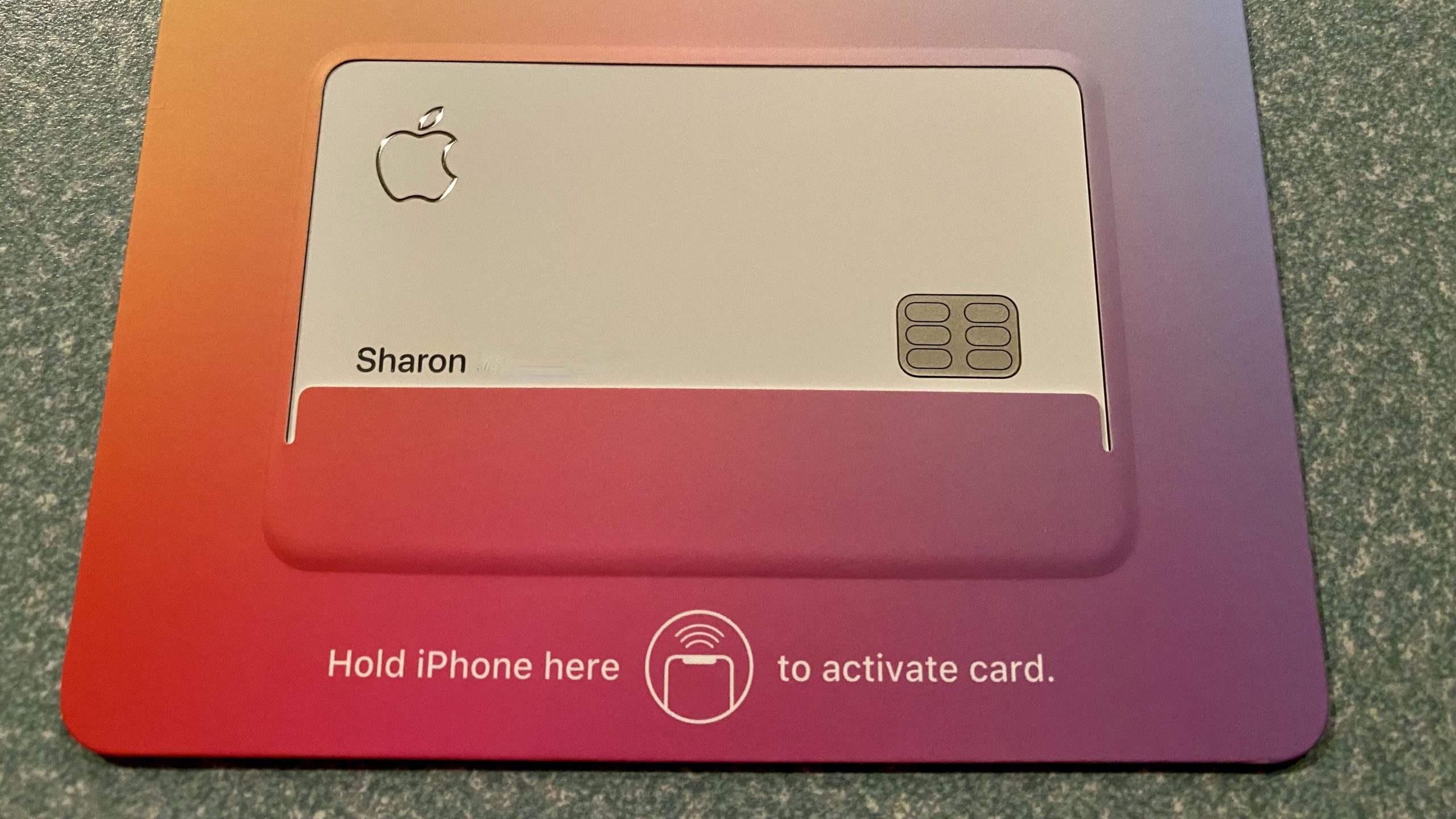

The Physical Card (and Why We Don’t Use It)

Even though we mainly use the card via Apple Pay, we did receive the sleek Titanium Apple Card in the mail. It looks cool — but since any purchase made with the physical card only earns 1% cashback, it now lives in a drawer.

Activation wasn’t super intuitive either. There were no links or codes — just a card and instructions to use your iPhone. You need to open the Wallet app and tap “Activate Card.” That’s it.

Everyday Use: Simple and Seamless

I like being able to tell Sharon to pay with her Apple Watch — she doesn’t need to worry about which card to pull out. Apple Pay earns 2% back on all purchases, which is perfectly fine by me.

Sure, I’d prefer she use the Amex Gold Card to earn 4X at grocery stores or the Citi Strata Premier for 3X at gas stations, but if earning 2% back makes her life easier, that’s a win.

Final Thoughts

The Apple Card isn’t the most rewarding credit card out there — especially if you’re chasing points and miles. But if you’re deep in the Apple ecosystem like we are, it’s surprisingly useful.

The ability to finance Apple products with 0% interest while earning 3% cashback upfront makes it a smart choice for those big-ticket tech purchases. Add in seamless integration with Apple Wallet, daily cashback, and ease of use with Apple Pay, and it fits right into our day-to-day life.

It’s not the flashiest card in our wallet (or technically, on our wallet), but when it comes to buying Apple gear, it’s hard to beat.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!.

This post first appeared on Your Mileage May Vary

{kind=link}

6 comments

Apple does offer third party payment options

I looked at different articles and couldn’t find any option for iPhones. We used Citizen One for our last phone and they took a CC for the automatic payment each month.

That’s kind of pathetic … sorry. Collecting a variety of cards to pay for consumption in installments (even if interest free and oh yeah cash back … what 3% on 1000 EUR that’s 30 EUR … winnnnnnner!!!) 🤦♂️

Yea, if you’re having to pay in installments then you probably should be questioning whether you should be buying it to begin with.

So what if Apple doesn’t allow installments, ATT and other carriers do. All my IPhones are paid over 30 months on my ATT account (most at very low price with an ATT $800-$900 credit for just committing to staying with them for 30 months). Frankly anyone that buys an iPhone directly from Apple is making a mistake and no 3% cash back or points/miles offer will change that.

But you are then married to ATT for the duration and ATT charges $5 per user per month for using a credit card. For those with multiple users who were used to 5X points, it is a loss of $200-$300 in point value per year. I for one will buy my next iPhone from Apple and chose the carrier that works for me. Everybody’s mileage varies.