Both Sharon and I currently hold JetBlue Plus cards from Barclays. While there are few hotel or airline co-brand credit cards we concurrently have, there are several reasons we both ended up with the same card.

Originally we both got the card for the new cardmember bonus.

- Sign-up bonus – The JetBlue Plus card often has a bonus between 60,000 to 100,000 points. For most redemptions, JetBlue TrueBlue points are worth around 1.4 cents each so that’s a great haul as far as signup bonuses go.

For the $99 annual fee, you get:

- Spending Bonus Categories – 6x points on JetBlue purchases and 2x points at restaurants and grocery stores

- Free First Checked Bag – The cardholder and up to 3 travel companions on the same reservations, who have purchased Blue fares, will each receive their first checked bag free on JetBlue-operated flights.

- 10% Rebate on Redeemed Points – You’ll get 10% of the points back every time you redeem them.

- Earn 5,000 Bonus Points Annually – Every year, after your account anniversary, you’ll receive 5,000 bonus points.

- 50% Savings on Eligible inflight purchases – When you pay for food or drink purchases in flight with your JetBlue Plus Card, you’ll save 50%.

- Earn JetBlue Mosaic status – After spending $50,000 or more on purchases annually with your JetBlue Plus Card, you’ll receive TrueBlue Mosaic status.

After the first year, there’s not much advantage for both of us keeping the card for these benefits as the checked bag and points rebate would apply if we only had one card in the family. We’re not making money on the 5,000 bonus points we’re buying for 2 cents each (which is less than we get for redemptions.)

There are two reasons I keep both cards:

- Barclays is notoriously stingy about approving people who have many open lines of credit. However, once you have an account and keep it for a while, it’s reportedly easier to get approved for a second card with a larger credit limit. This was true for both Sharon and me when applying for cards from Barclays.

- There are semi-regular bonus offers sent out to co-brand cardholders.

In fact, we were targeted for a 60,000 bonus point offer last fall if we spent $3,000 on the card over 3 months. You better believe I took advantage of that one.

Both Sharon and I received emails from Barclays with spending offers on our JetBlue Plus cards.

One of the offers will be easy to max out for some non-bonused spending.

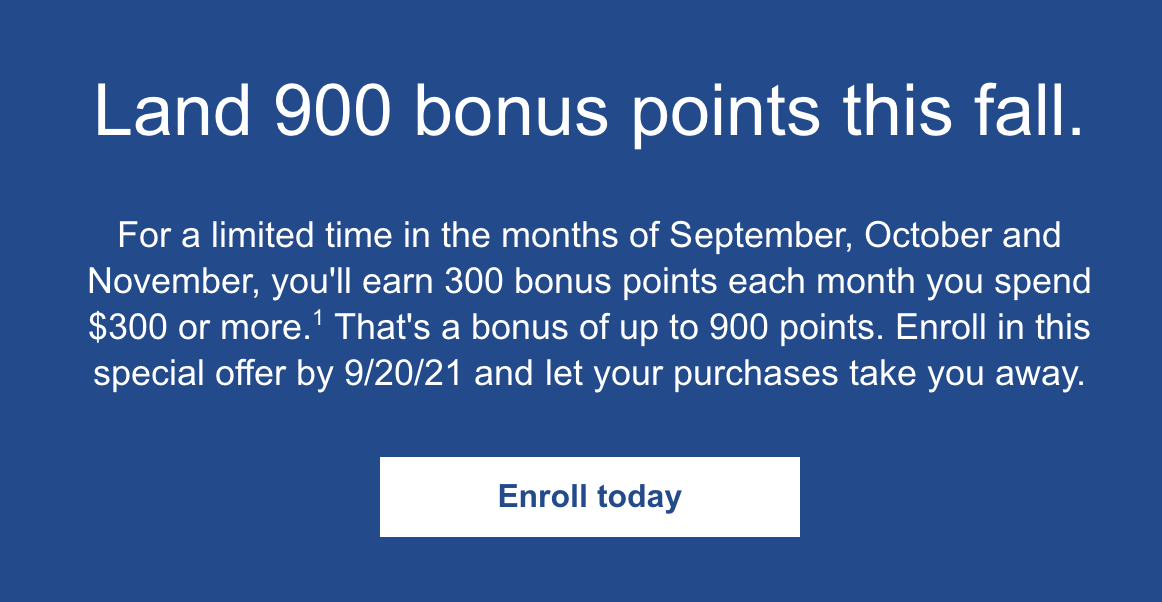

For a limited time in the months of September, October and November, you’ll earn 300 bonus points each month you spend $300 or more.

That’s like earning 2x JetBlue points for $300 in purchases for 3 months. 2.8% return for everyday spending is better than what I get back from our 2% cashback Fidelity card. I like to put spending on the card when I get these offers as it keeps the account active and hopefully will attract future offers.

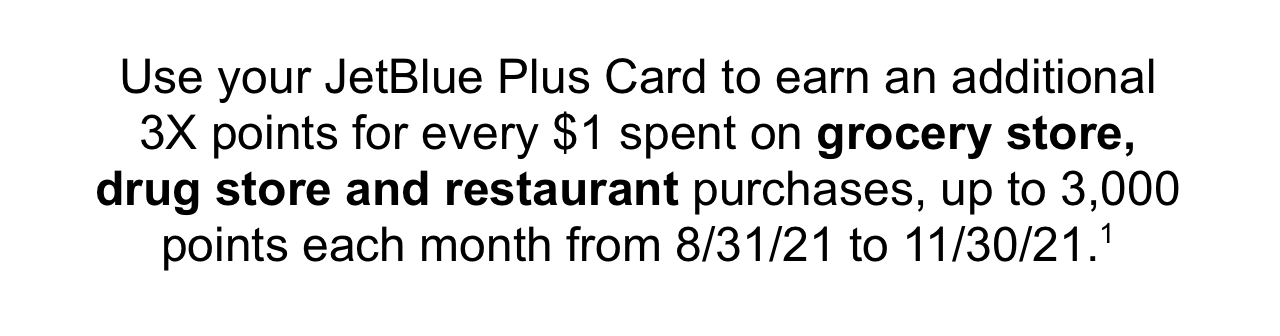

The offer on the other card is more lucrative but has more restrictions.

Use your JetBlue Plus Card to earn an additional 3X points for every $1 spent on grocery store, drug store and restaurant purchases, up to 3,000 points each month from 8/31/21 to 11/30/21.

An interesting quirk about Barclays offers is that the bonus points are in addition to what you’d usually earn with the card. With this offer, you’ll earn 5X points at restaurant and grocery stores and 4X points at drug stores every month for the first $1,000 of combined spending.

That’s better than the best-earning card I currently hold for each category. My AMEX Gold card earns 4X points at restaurants and grocery stores and the Chase Freedom Unlimited earns 3% (or 3 Ultimate Rewards) at drugstores.

I could always just earn the Amex Membership Rewards points and transfer points to JetBlue if I need them but then I’d have to pay the AMEX excise tax due when transferring points to US airlines.

There’s an argument to make that by earning JetBlue points, I’m putting myself in jeopardy if there’s a sudden devaluation. I usually redeem JetBlue points for Blue Fares on domestic trips so I’m not worried about a massive shift in the program as it’s already revenue-based. If I were saving points looking to redeem for a flight in Mint Class to London, it would be more of a consideration.

Did anyone else get offers on their JetBlue or other Barclays co-brand cards? How are they compared to ours?

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and get emailed notifications of when we post. Or maybe you’d like to join our Facebook group – we have 23,000+ members and we talk and ask questions about travel (including Disney parks), creative ways to earn frequent flyer miles and hotel points, how to save money on or for your trips, get access to travel articles you may not see otherwise, etc. Whether you’ve read our posts before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}