To optimize our financial rewards, I apply for credit cards with large bonuses and higher-than-average spending requirements when we have significant expenses on the horizon. We can usually satisfy a three-month spending threshold of $3,000 to $5,000 by transferring all our usual expenses to a new card. If the spending requirement exceeds this amount, we get creative and devise practical ways to reach the bonus threshold. Given our expectation of several significant expenses in the coming months, I chose a card with a higher spending requirement than usual to maximize our rewards.

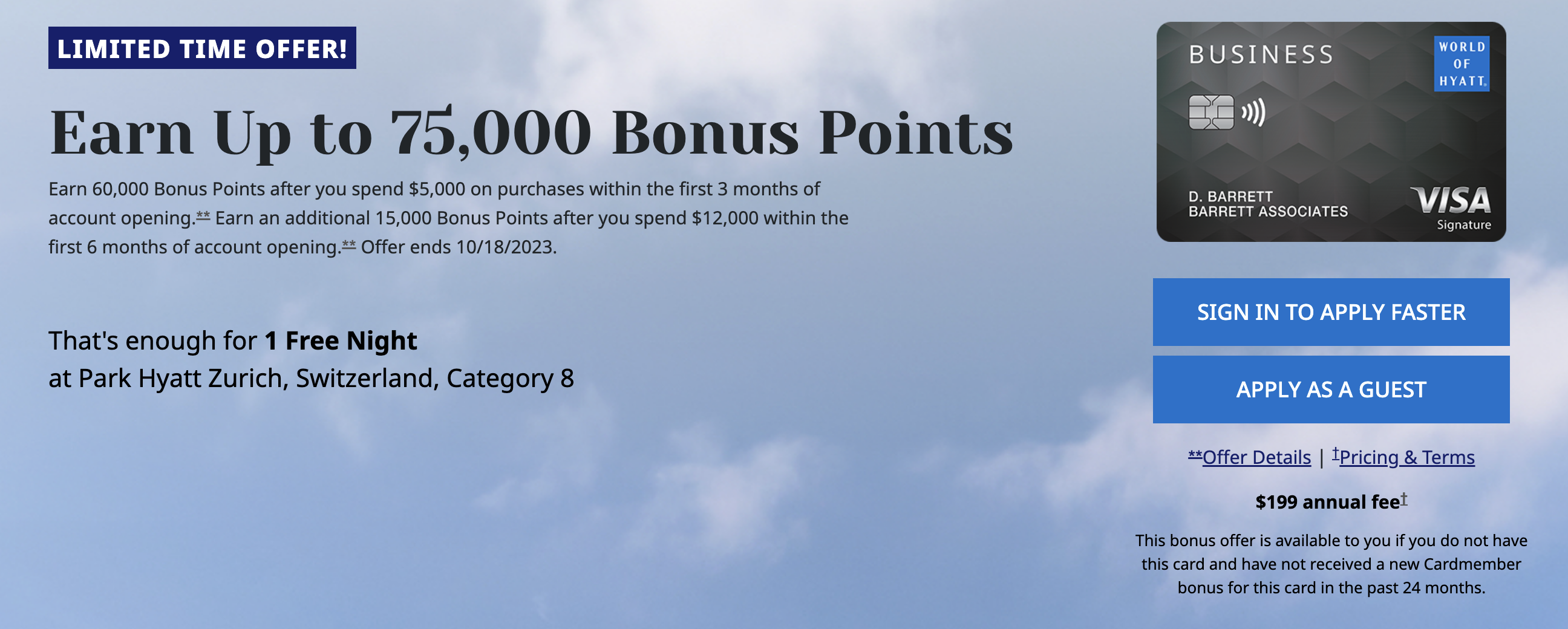

The Chase World of Hyatt Business card offered a 75,000-point bonus when we applied. You’d earn 60,000 points after spending $5,000 in the first 3 months and 15,000 extra points if you spend $12,000 in the first six months.

When Sharon applied for a new credit card, she already had five Chase personal cards and two Chase business cards. I was a bit concerned about her chances as we were nearing the maximum amount of credit that Chase typically offers. Nonetheless, I realized she was still under the 5/24 limit, so there wasn’t much harm in applying. The potential reward of 75,000 Hyatt points was too great to pass up, especially since it could pay for another trip to the Grand Hyatt Kauai.

View from our balcony at the Grand Hyatt Kauai

She received an instant approval for the card. However, the credit limit on the card was only $5,000, which is the lowest we have on any credit card from Chase.

It also makes spending $5,000 in three months and $12,000 in six months a little more challenging.

A few of the big expenses came shortly after receiving the card, and we charged $4,500 to it within the first two weeks. I promptly paid off the balance as soon as the statement closed so we could meet the requirement of $5,000 and receive the initial 60,000 points. During this period, we traveled quite a bit, and I opted to use our travel cards, such as the Sapphire Reserve and AMEX Platinum, instead of bringing along this card.

When we arrived home, I attempted to charge $750 to the card, only to have it declined. After checking our email and the Chase app, I found no mention of a fraud alert. I then tried a smaller purchase from a different online vendor, but the card was again denied. Finally, I suggested Sharon try using the card for her purchase at the local Walmart. Unfortunately, the card was declined again.

I searched for any fraud alerts on the Chase website, Chase app or text messages, but found nothing. The only option left was for Sharon to call Chase. I don’t enjoy making this request, as she dislikes making phone calls, especially to banks, to discuss credit cards, since she’s not an expert in that area.

When I explained that if she didn’t call, we wouldn’t get the 75,000 World of Hyatt points and wouldn’t be able to stay at the Hyatt in Kauai, she reluctantly dialed the customer service number on the card.

It was a short wait to talk to a representative to ask why our card with a zero balance kept getting denied everywhere but we have no message from Chase about why. I was listening to the conversation, and after the Chase rep verified Sharon’s information and confirmed that the charges on the account were ours, they lifted the hold on the account.

They explained that the charges on the account were suspicious and flagged as possible fraud. Since we confirmed the charges were legitimate, the hold was taken off the account.

We only had a few weeks to complete the final bit of the spending requirement, but I was happy to see the 60,000 points are now in Sharon’s World of Hyatt account.

We have another 3 months to spend another $7,000 for an additional 15,000 points. That’s more than 3 Hyatt points per dollar (1 regular plus 2 bonus points) and should get us almost 6 cents per dollar or more in return for a decent Hyatt hotel stay.

Has anyone else had this happen where a bank shut down one of your cards, didn’t tell you and the only way to find out was to call and see why it kept getting declined?

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

2 comments

Not an exact comparison but I have had Chase decline my “card not present” transaction when I tried to book online directly with an international hotel. I got around it by booking the same hotel through Expedia using my Chase card. Chase also declined my attempt to pay for an eVisa through an international entity, I used Amex and the transaction went through. In a “card present” transaction, I’ve had no problems with Chase domestic or international.

I recently got approved for the Chase United card (6th personal card – no business cards). CL was $16.5.

In a trip to Walmart a $270 charge was declined. Luckily I got a text instantly. I answered YES, that it was me, and tried the charge again – this time successfully. I have always found Chase good at texting at the time of any decline.