I’ve been earning points and miles with credit cards for over twenty-five years. I originally had an older version of the American Express Gold Card that earned 1.5x on travel purchases. Any bonus category was rare back then, so earning extra Membership Rewards points for my trips was fantastic. I eventually got a Diners Club card because once I was old enough to rent a car (25 years old), the primary renter’s coverage was very important to me (being the son of an insurance claims adjuster helps you set priorities).

I’ve seen travel cards come and go. And then, about fifteen years ago, I started getting serious about points and miles. I cautiously waded into the world of credit card sign-up bonuses.

Each card I signed up for had a specific purpose. The Alaska Airlines card was to get a $99 companion ticket I could use for our anniversary trip to Hawaii. The Starwood AMEX had flexibility with the number of airline transfer partners available. The Sapphire Preferred was our entry into the world of Chase Ultimate Rewards opportunities. When I signed up for each card, spread out over several months, I made sure I’d be able to easily meet the spending requirements without having to spend any extra money over our budget. When I knew I had a large purchase coming, I’d pick out a new card so we could take advantage of an extra sign-up bonus.

I also made sure I was getting extra points where available. Shopping portals. AMEX offers. Bonus categories. Special offers. Retention offers. I looked into them all. When examining if I should keep a card, I always looked to see if something about it would make sense for me not to cancel it. I’ve always wanted a good relationship with the banks because I need them to finance a car and get a mortgage.

Even with taking several trips that cost a boatload of points, I still have over two million of them spread over all of our accounts. Not too bad. It’s more than enough for whatever trip we’d ever want to take and still lets me redeem 100,000 points for last-minute tickets for a family emergency without batting an eye.

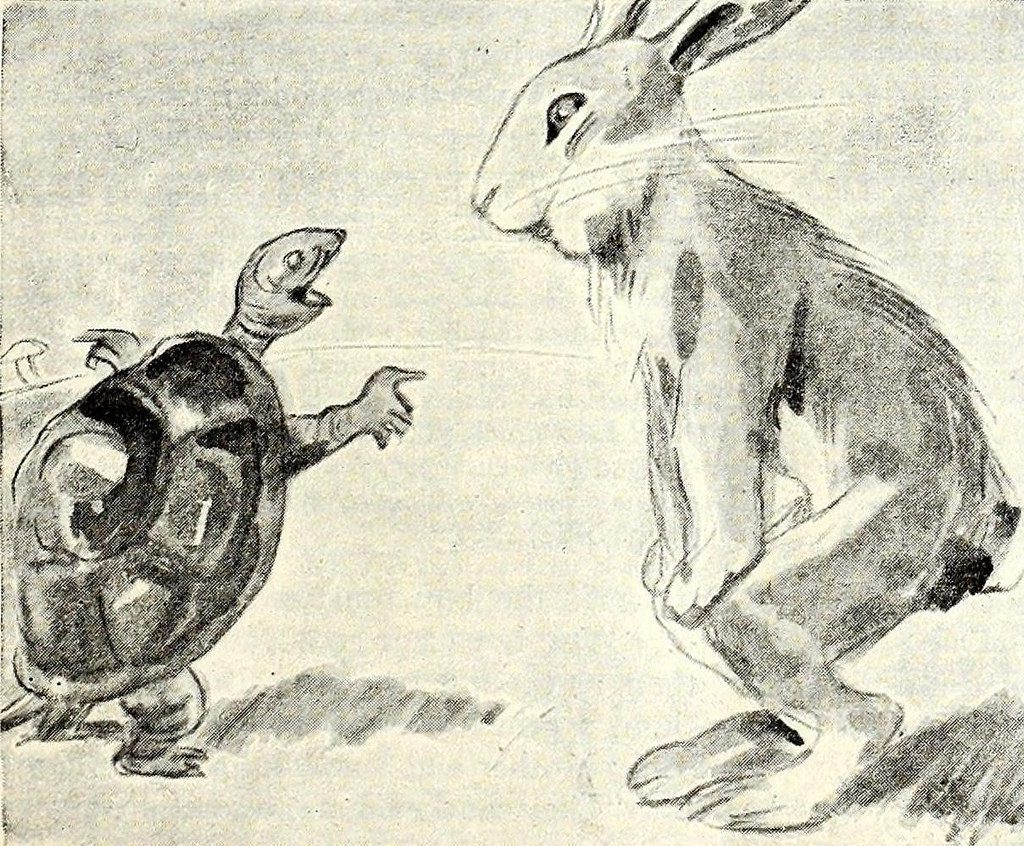

So, who’s the hare if I’m the tortoise in this game?

While researching this post, I read plenty of bulletin boards, Facebook, Twitter, Reddit posts, and other websites and have seen many things that make me shake my head.

They usually say something like this:

- I just signed up for ten credit cards; when will I get my miles?

- I bought $10,000 in gift cards; what can I do with them?

- I charged $5000 a week to my card, paid it off, and charged another $5000 every week for 3 months. The bank (Chase, AMEX, take your pick) shut down my accounts. Why?

- I signed up for a card and got the signup bonus. How soon can I cancel the card?

- Can I sign up my pets as authorized users on my account?

- I signed up for 25 cards over the last eighteen months. What card should I sign up for next?

There are many foolish things that you see every day. People are doing things they have no idea about but may have a long-lasting effect on their financial well-being.

Some people can do all of the above things (well, not signing up your pets) and make them work. I’ve met them. They are brilliant people who know the risks involved with their activities. For example, Greg from Frequent Miler used multiple credit card bonuses over seven months to earn 1.2 million Virgin Atlantic miles and spent a week on Richard Branson’s Necker Island.

I’m not against those who can push the envelope and see what’s possible. I’m just not one of those people. I want to sail under the radar, picking up fruit when it’s plentiful and scrambling around to pick up the scraps when pickings are slim, surviving off the stash I’ve saved over time.

When collecting points and miles, remember these two quotes:

“Pigs get fat. Hogs get slaughtered.”

“The early bird may get the worm, but the second mouse gets the cheese.”

I might miss out on a lucrative back-door offer to earn a ton of miles. That’s OK. I can live with losing out on some extra miles. I’m happy going along slow and steady, taking my time, and not stretching myself too far. Maybe that’s not your style. That’s OK—Your Mileage May Vary.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

5 comments

Oh please . If you knew you could print 100 million MR in one year, but then never ever have an Amex account again, are you really saying you wouldn’t jump at the chance? Even though it would cash out to $1.1mm ? Any sane person would take that trade in an instant

But that isn’t a practical situation so quit trying to make it so. Personally I like his approach. The max spend, churners and gift card shysters all deserve, IMHO, to have their accounts closed, points clawed back and put on that bank’s “never again” list. I have $200,000 a year in organic spend based on my normal lifestyle so don’t have to take any questionable shortcuts

Patience grasshopper

You stole my thunder. Rick Ingersoll who used to blog as Frugal Travel Guy used that same quote “Pigs get fed; hogs get slaughtered”. There were a few other bloggers out there that would brag and offer advice how to get 2, 3, 4 of the same cards doing apparama’s, often times getting there accounts shut down for doing so.

Having recently retired, I’m taking the tortoise approach. I still apply for cards and take advantage of the lucrative deals. My aim is to stay conservative so I can use the millions of miles and points I have accrued. Right now I’m on a 2 1/2 week driving vacation and I’m doing it on points and free night certificates. Nothing wrong with that.

There are aggressive churners and there are old churners but very few aggressive old churners. Live fast die young.