One of the benefits of paying for travel with a Chase Sapphire card is the excellent travel coverage in case something goes wrong. After charging your trip to the card, you’ll receive coverage for trip delays, trip cancellation/interruption, delayed baggage, and lost baggage.

One additional perk that comes with the Sapphire Reserve and Ritz-Carlton cards is emergency evacuation coverage. When you pay for a trip with either of those cards, you’re eligible for up to $100,000 in coverage if you need to be transported due to medical reasons. It’s not a primary reason to hold the card, but it’s reassuring to know it’s there if needed.

If we’re planning a major trip, I’ll often purchase a separate travel insurance policy that includes both evacuation coverage and medical insurance. And yes, you really do need to buy medical insurance when traveling outside the USA.

Chase Changed Its Exclusion Policy

In the past, Chase published a list of countries where their emergency evacuation coverage wouldn’t apply. That’s no longer the case. The updated policy now reads:

Emergency evacuation and transportation, and repatriation of remains services may not be available in countries where the US Department of State has a current travel warning issued or in countries where the US Department of the Treasury’s Office of Foreign Assets Control (OFAC) has active economic or trade sanctions or that are subject to other applicable trade or economic sanctions, laws and regulations. The Covered Traveler should consider the restrictions on services related to international laws on sanctions before planning the Covered Trip. Additionally, no services will be available in any country or territory where the existing infrastructure is deemed inadequate by the Emergency Evacuation and Transportation service provider to guarantee service.

This change gives Chase far more flexibility. Instead of maintaining a fixed exclusion list, they can now rely on external advisories—like those from the U.S. Department of State or OFAC—to determine when coverage “may not be available.”

What Does That Mean for Travelers?

This update reflects a shift from listing named countries to referencing government advisories. That gives Chase the ability to adjust in real-time as conditions change, without needing to reissue policy documents each time a country becomes riskier to visit.

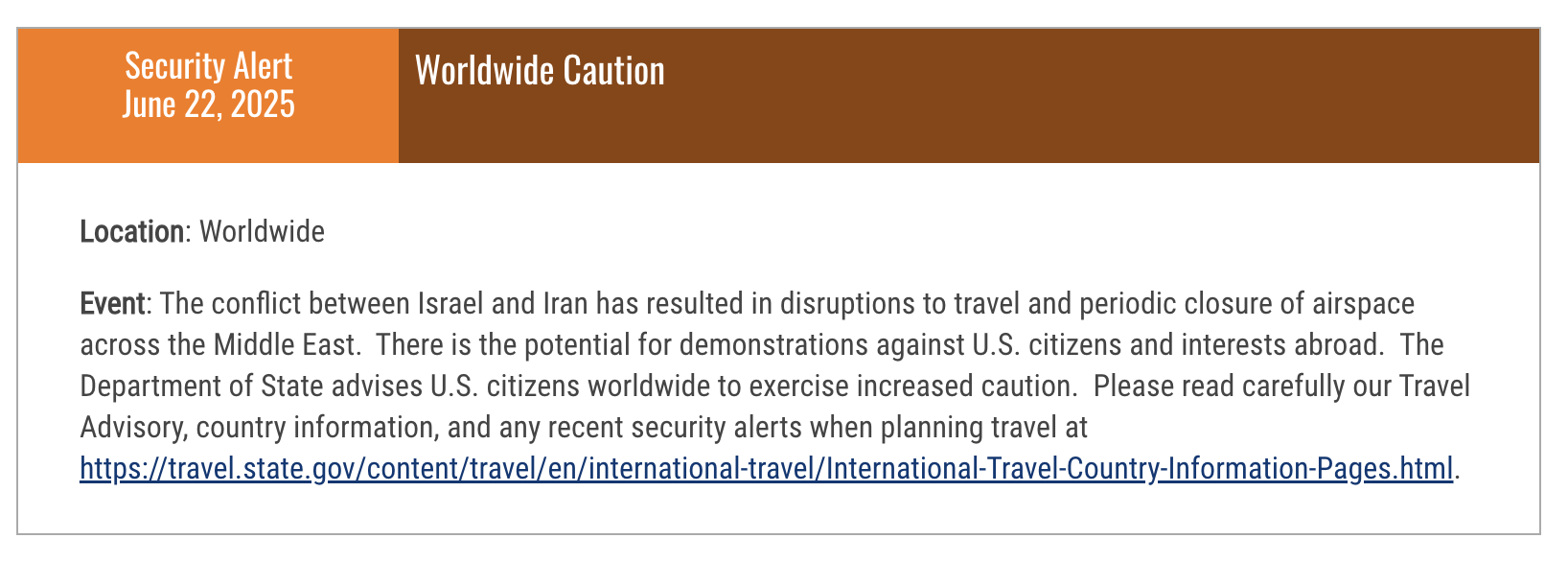

And the global travel landscape is changing quickly. As of the writing of this post, the State Department has issued a Worldwide Caution for U.S. travelers due to heightened tensions and the risk of violence against Americans overseas.

While Chase’s policy excludes destinations under travel warnings, it’s unlikely they meant to restrict coverage on all travel during a worldwide caution. That’s why their use of the phrase “may not be available” is doing a lot of work here. It leaves them flexibility to deny coverage without promising exactly where the line is drawn.

What level of warning counts? A Level 1 advisory simply means exercising normal precautions. A Level 4 means “Do Not Travel.” The benefit guide doesn’t specify, which adds to the uncertainty.

Final Thought

While it’s great that Chase offers this benefit, don’t assume you’re fully protected, especially in high-risk areas or during times of global instability. The fact that Chase no longer publishes a specific exclusion list means you’ll need to do your own homework. Check State Department advisories, understand how your destination is categorized, and seriously consider supplemental insurance when traveling internationally.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}

2 comments

Thanks for posting this important information. I have always paid for medical evacuation insurance on my own because I don’t want to take the risk in case Chase does not want to pay. Hopefully this is something that I will never ever need.

So there’s no more countries that aren’t covered like there used to be? AmEx currently doesn’t cover Australia and New Zealand for example. And there were definitely some European countries that Chase didn’t cover last year.