After deciding not to keep the Citi Prestige® Card, I had three options: try for a retention offer, downgrade to a no-annual-fee card, or cancel the card entirely.

Retention Offer

In my post about canceling the card, I calculated that I’d need to save an additional $245 in benefits to break even. Therefore, any retention offer would need to meet or exceed this value without a hefty spending threshold. However, reports suggested that many cardholders weren’t receiving offers, so while I planned to inquire, I wasn’t counting on one.

Canceling the Card

Canceling the card was an option, but it comes with significant downsides, particularly with Citi ThankYou® points. Unlike Chase Ultimate Rewards® and Amex Membership Rewards®, Citi doesn’t allow you to keep ThankYou points alive if you cancel the card that earned them. Points expire 60 days after cancellation.

To avoid losing the points, I’d need to transfer them to a Citi partner airline or hotel or use them for travel via the Citi Travel website. However, canceling a Citi card outright is usually unnecessary, as Citi is one of the most lenient banks when it comes to product changes.

Product Change/Downgrade

Citi allows cardholders to change to other cards within the same family. For example, I downgraded from the Citi Prestige® Card to the Citi Double Cash® Card, which earns 2 points per dollar (one when you make the purchase and another when you pay the bill). The Citi Double Cash® Card is a no-annual-fee option, while the Citi Strata Premier® Card is needed to transfer points to travel partners.

Other options that preserve your points include the Citi Rewards+® Card, Citi ThankYou® Preferred Card, and the AT&T Access Card. Occasionally, you may also be able to transfer to a different card family. This post on AwardWallet lists many of the Citi cards you can product change to.

Citi Glitches

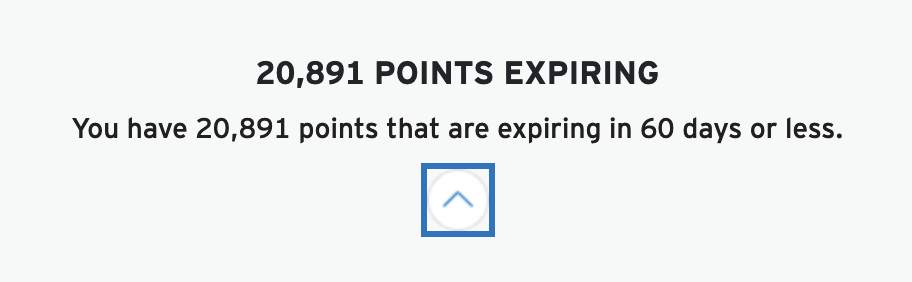

While changing cards over the phone was easy, Citi’s IT system had a couple of quirks. Initially, my points balance on the Citi Double Cash® Card was zero, but I knew from this Frequent Miler post that it can take time for points to appear after a product change. They eventually showed up, but another issue arose: my points showed an expiration date of 60 days, the typical timeframe after canceling a card.

According to Greg from Frequent Miler, this is a common issue:

“Soon after product changing from one ThankYou card to another, you can log into your account and see that your points will expire within 60 days. Don’t panic. Your points won’t really expire. Wait a few more weeks, and you’ll see that the points no longer have an expiration date.”

I’ll monitor my account to ensure this happens. I’ll also watch for a refund of the Citi Prestige® Card’s annual fee, as Citi typically refunds it if you cancel or downgrade within 37 days of the fee being billed.

Final Thoughts

Downgrading from the Citi Prestige® Card to the Citi Double Cash® Card made the most sense, especially since we already have the Citi Strata Premier® Card. Now, we earn 2X ThankYou® points on all purchases. While the process wasn’t without glitches, reading up on it beforehand helped ease my concerns about losing points.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}