Amex Offers can be a great way to save money, but they’re not as simple as “add the offer, use the card, get the credit.” Sometimes, one small detail buried in the terms can make the difference between saving money and getting nothing.

I recently got a $100 reminder of that.

And this wasn’t one of those cases where I forgot to add the offer, used the wrong card, booked through a third party, or missed the expiration date. I thought I had done everything correctly. I added the offer to my American Express Platinum Card, booked directly with the merchant, and used the enrolled card for the reservation.

But one detail kept the credit from posting.

The AMEX Offer That Looked Like An Easy Win

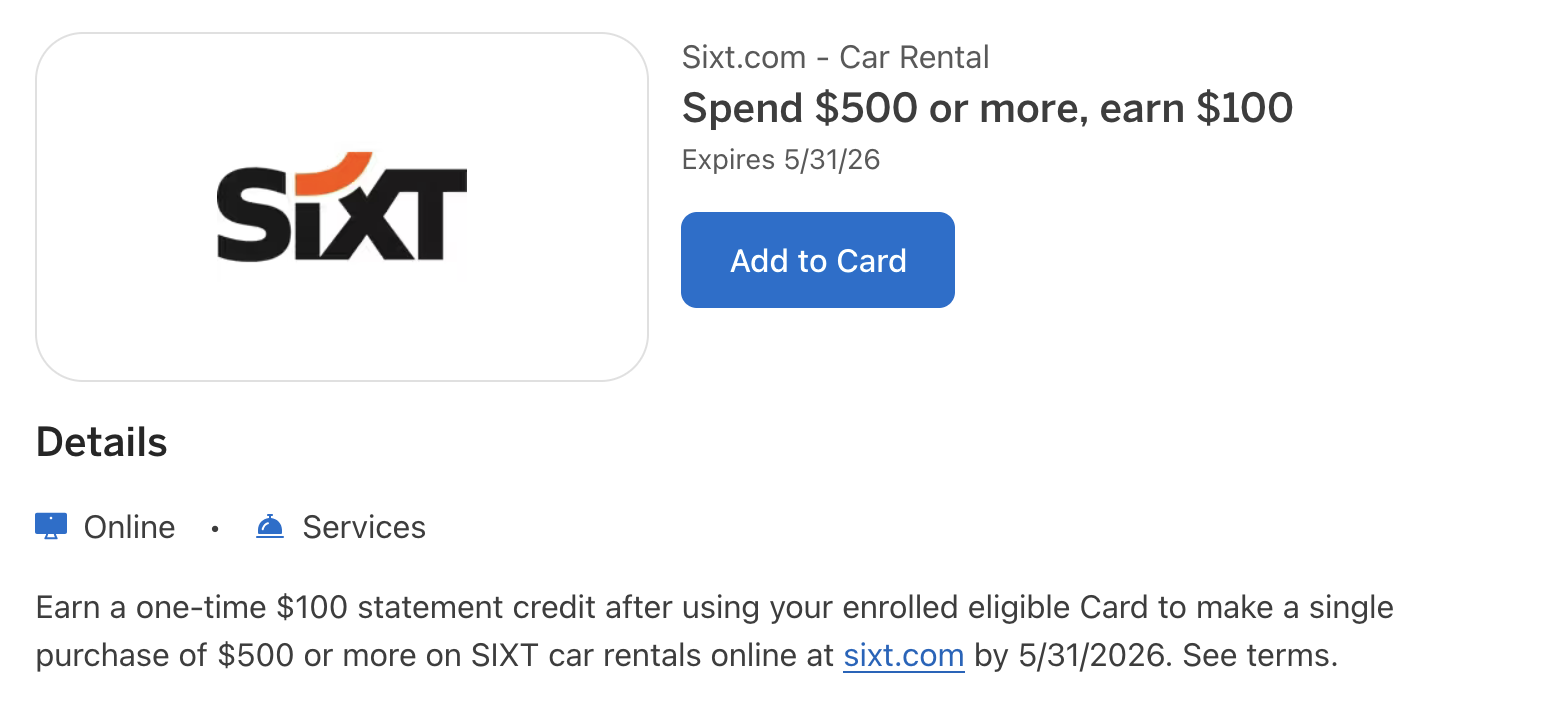

The offer was for SIXT car rentals:

Spend $500 or more, earn $100 back

That’s a meaningful offer. If this had been a $5 credit, I probably would have shrugged and moved on. But $100 is enough to care about, especially when it influences which card you use for a purchase.

We were renting a car in Germany, and the rental would cost more than $600. I booked the reservation directly through Sixt.com, the price displayed in U.S. dollars, and I used my enrolled American Express Platinum Card to hold the rental.

I did not prepay the reservation. The card was on file for the booking, and I expected the final charge to count once the rental was paid.

That’s where things got messy.

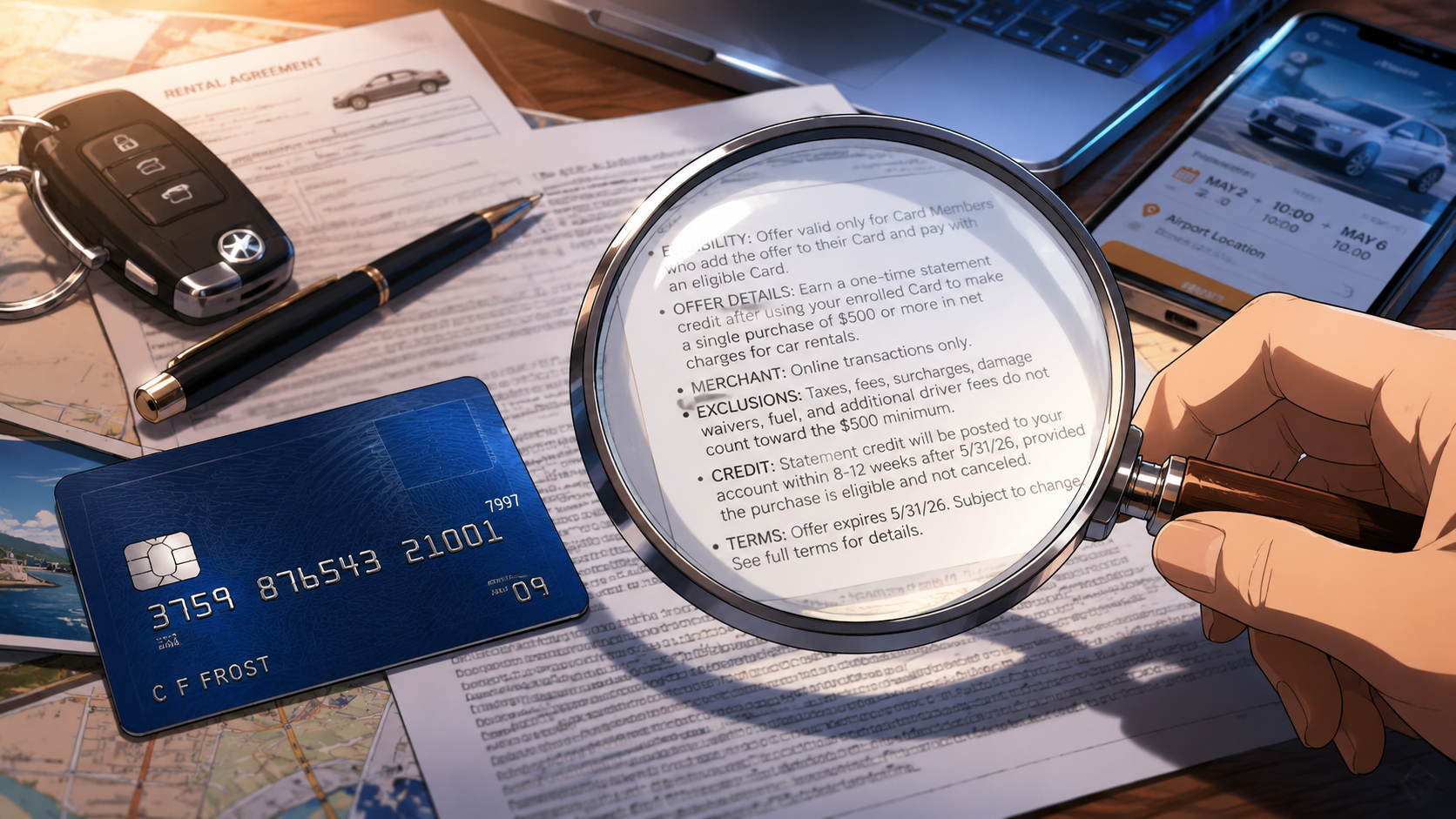

The Fine Print That Mattered

Here’s the important part of the offer terms:

Offer valid on SIXT car rental purchases made online only at US website sixt.com. Eligible rentals must be paid for by 5/31/2026 in order to qualify. Offer valid only on purchases made in US dollars.

At the time, I focused on the big-picture items. I booked directly through Sixt.com. The rental was over $500. The price was shown in US dollars. The Amex Offer was added to the card. And the same Amex Platinum Card was attached to the reservation.

That seemed good enough.

Except it wasn’t.

Because I didn’t prepay, the actual charge happened later, connected to the rental in Germany. And when it posted to my Amex account, it posted as a foreign transaction in euros.

That one detail was enough to make the purchase ineligible for the offer.

What American Express Said

After waiting more than a month without seeing the credit post, I contacted American Express via chat. Their response was that the charge didn’t qualify because it was processed as a foreign/non-U.S. transaction, while the offer required purchases to be made in U.S. dollars through the U.S. website.

That was frustrating because, from my end, I had booked through Sixt.com and the price had been displayed in U.S. dollars when I made the reservation. But since the actual payment was posted in euros, it didn’t meet the terms.

I pushed back, but the answer didn’t change. American Express said the merchant sets the offer terms and that they can only track whether a charge meets those terms. In other words: no exception.

In Retrospect, There May Have Been One Way Around It

Looking back, it appears the only way this offer works in this sort of situation is to prepay on the website. But that’s not really what it says. If that’s the deal, then just say so instead of dancing around the point.

While I avoid prepaying for rentals, this situation may have been different. If paying in advance in U.S. dollars had triggered the $100 Amex Offer, it might still have been worth it.

Still, it’s something I’ll think about the next time an offer requires payment on the website in U.S. dollars.

The Real Cost Was More Than $100

Losing the $100 statement credit was annoying enough. But that wasn’t the only cost.

Because I was chasing the Amex Offer, I used my Amex Platinum Card for the rental. That meant I earned only 1X Membership Rewards points on the purchase. I also passed up the chance to use another card that would have offered better rental car coverage and a better earning rate.

That’s the part that stings.

I didn’t just miss out on an offer. I made a card choice based on an offer that ultimately didn’t pay out.

The Lesson: Reservations And Final Charges Aren’t Always The Same Thing

This is the part that’s easy to miss. With hotel and rental car offers, making a reservation and making a qualifying purchase are not always the same thing.

You might book on the U.S. website. You might see prices in U.S. dollars. You might use the enrolled card to hold the reservation. But if the actual charge is processed later by an international location, in a foreign currency, the offer may not trigger.

That’s the trap.

Before letting an Amex Offer decide which card you use, it’s worth checking:

- Does the offer require purchases in U.S. dollars?

- Does the offer require pre-payment online, not just booking online?

- Will the final charge be processed by a U.S. merchant or a foreign location?

- Are you paying now, or are you only holding the reservation?

- Would you still want to use that card if the offer doesn’t work?

That last question is the one I’ll pay more attention to going forward.

AMEX Offers Are Useful, But They’re Not Foolproof

This is where Amex Offers have started to feel more like the rest of the pack.

For years, American Express had a reputation for premium service, especially on high-annual-fee cards. But when it comes to these merchant offers, the terms are the terms. Even if you’re paying almost $1,000 a year for a card, don’t assume American Express will step in and fix a technicality.

That doesn’t mean Amex Offers aren’t worth using. They can still provide real savings. But they require more attention than just clicking “Add to Card” and assuming the credit will appear.

Final Thought

This was a $100 lesson in reading the fine print on Amex Offers. I thought I had done everything right: I added the offer, booked directly with SIXT, used Sixt.com, attached the enrolled card to the reservation, and spent more than $500.

But because the final charge was processed in euros instead of U.S. dollars, the offer didn’t trigger.

The lesson isn’t that Amex Offers are bad. It’s that they’re not automatic savings, and they’re not always as straightforward as they appear. Before letting an offer decide which card you use, make sure the purchase will actually qualify—and make sure you’d still be happy using that card if the credit never posts.

Because sometimes the fine print doesn’t just cost you the offer. It costs you the better card you could have used instead.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}