When we travel within the U.S., I don’t give much thought to travel insurance before the trip. I make sure to use a credit card with good travel protections, and if I rent a car, I use a card that provides primary coverage for damage to or theft of the rental vehicle. For medical coverage, I’ll keep my health insurance card in my wallet in case I get sick or, even worse, have an emergency.

Traveling outside the United States requires a little more preparation. You need to reconfirm your arrangements, make sure you have the necessary travel documents and visas, and arrange for your mail to be held, your pets to be looked after, and everything else that crosses your mind before an international trip.

With all of that going on, it can be easy to forget about something else you may need: travel medical insurance.

The coverage provided by your regular health insurance can vary significantly once you leave the United States. Some plans provide limited emergency coverage, some treat foreign medical care as out-of-network, and others may not cover it at all. Even when treatment is covered, you may have to pay the provider out of pocket and request reimbursement later.

Original Medicare generally provides very limited coverage outside the United States, although there are a few specific exceptions. Some Medicare Advantage plans include emergency or urgent-care coverage abroad, so you need to check your individual plan. Certain Medigap policies may also cover part of the cost of qualifying foreign emergency care, subject to deductibles, time limits and a lifetime benefit limit.

There’s also the possibility that you could need medical transportation or evacuation. Even a health insurance plan that covers treatment overseas may not pay for transportation to another hospital or back to the United States.

Medical care outside the U.S. may cost less than what we’re used to paying here, but I still don’t want to pay out of pocket if I need to see a doctor while I’m away. That’s why I purchase a separate travel medical policy when we leave the country.

How to find an insurance company

I don’t know about you, but I really don’t want to spend time visiting multiple insurance company websites and comparing policies. I’ve found that, in this instance, using a comparison-shopping website works best for my needs.

For many trips, I’ve used InsureMyTrip.com. I can’t say whether it’s the best, easiest or cheapest comparison website, but I’ve consistently found policies that fit our trips.

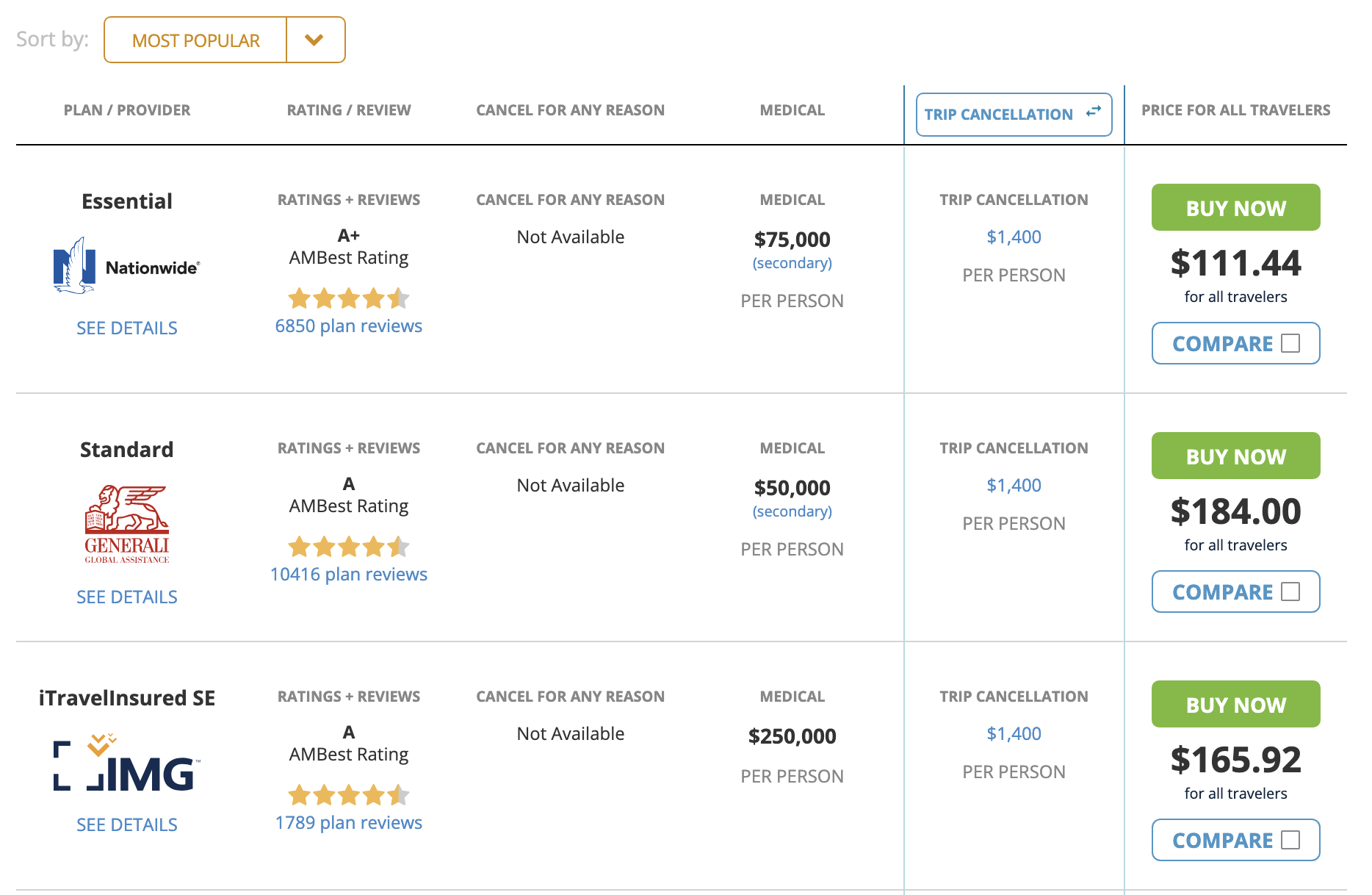

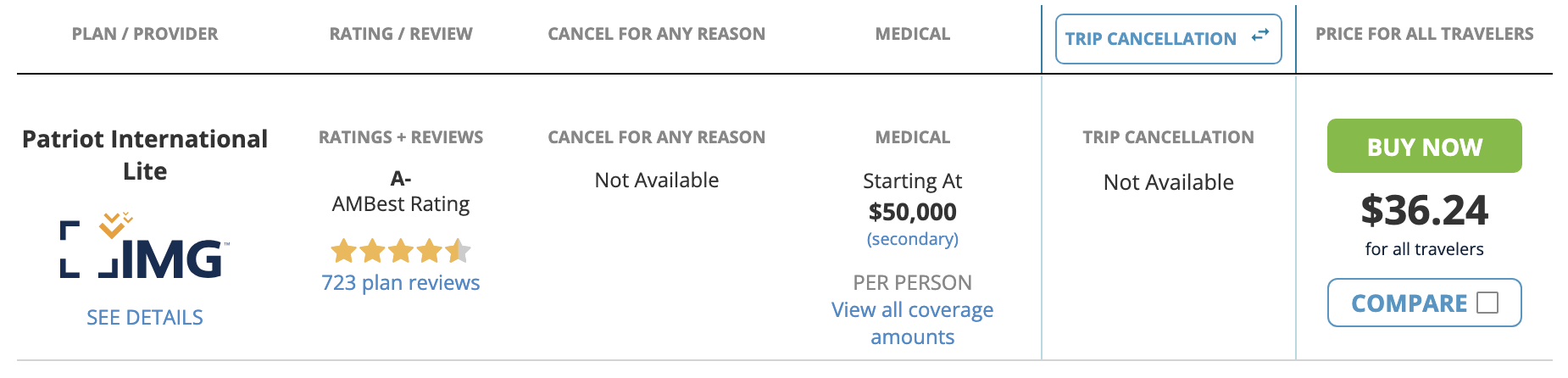

After entering some basic information about the travelers and the trip, the website shows policies from multiple insurance providers. You can then compare coverage limits, deductibles and prices without visiting each insurance company separately.

The default search generally shows comprehensive policies, which can include protections such as:

- Trip delay, cancellation and interruption

- Baggage delay or loss

- Accidental death

- Medical evacuation

- Emergency medical and dental coverage

The site makes it easy to compare plans from different providers, or even several options from the same company. For the trip shown in these screenshots, I already had many travel protections from using our Ritz-Carlton Card to pay for the reservations, so I narrowed the search to policies focused on medical coverage.

Medical coverage policies

Eliminating the broader travel protections brought down the price significantly. The rates shown in this screenshot were for the two of us on a five-day trip several years ago, so they shouldn’t be treated as current quotes. I’m including them to show the type of comparison the website provides.

For that particular trip, the cost of adding medical coverage was relatively small compared with the overall cost of traveling. That won’t always be the case, since premiums can vary based on your age, destination, length of the trip, coverage limits and deductible.

Some destinations or visa categories also require travelers to carry specific medical or travel insurance, so it’s important to check the current entry requirements for your trip.

If you travel outside the U.S. several times a year, it may make sense to consider an annual multi-trip policy. Just make sure to compare the coverage limits, the maximum length allowed for each trip and whether trip cancellation is included.

Final Thoughts

I wouldn’t think of traveling outside the United States without having medical coverage. That doesn’t mean I haven’t forgotten about it until the day before a trip. Fortunately, buying a basic policy is usually quick and straightforward, although some policies must be purchased before departure and certain benefits may only be available if you buy coverage soon after making your first trip payment.

I’m sure I might find a slightly lower price if I visited every insurance company’s website and compared policies myself. But since the coverage I’ve purchased has generally been reasonably priced, this is one instance where I’m happy to save time, even if it means paying a few extra dollars.

While I usually use InsureMyTrip, other travel insurance comparison sites, including Squaremouth and TravelInsurance.com, work similarly. Regardless of which website you use, compare the medical limits, evacuation coverage, deductibles, exclusions and rules involving pre-existing conditions before buying.

The cheapest policy may not be the one you want if you actually need to use it. The important thing is to understand what your regular health insurance covers outside the United States and make sure any gaps are covered before you leave.

Want to comment on this post? Great! Read this first to help ensure it gets approved.

Want to sponsor a post, write something for Your Mileage May Vary, or put ads on our site? Click here for more info.

Like this post? Please share it! We have plenty more just like it and would love it if you decided to hang around and sign up to get emailed notifications of when we post.

Whether you’ve read our articles before or this is the first time you’re stopping by, we’re really glad you’re here and hope you come back to visit again!

This post first appeared on Your Mileage May Vary

{kind=link}